Open or contribute to a CIBC Tax-Free Savings Account (TFSA) Tax Advantage Savings Account®

Print

PrintTrademarks and disclaimers

† Interest is calculated on the full daily closing balance and is paid monthly. The interest rates quoted are annual rates. The Regular Interest Rate may change at any time without prior notice.

Please wait, loading your information.

Are you sure you want to cancel? If you cancel this application, all your information will be lost permanently.

- Your contribution will be dated today or the next business day. However, funds may take up to 2 business days to be transferred from your deposit account to your TFSA account. Provincial holidays are considered business days when determining a contribution date. Saturday, Sunday and federal holidays are considered non-business days.

- Applications submitted before 11:59 p.m. ET on December 31 of this year will be accepted for processing as part of your TFSA contribution for this year.

We use multiple layers of protection when you access your online banking or investment accounts. Learn more

Your Social Insurance Number (SIN) is a 9 - digit number issued by the government of Canada that is required in order to register your plan.

All printed and mailed information received from CIBC will be in the language you selected.

Note that we need your home address, not a P.O. Box number. If you wish to add a mailing address, please call 1-888-872-2422 or visit your local branch.

You must provide your current occupation to apply. In order to add or update you must select an occupation field first.

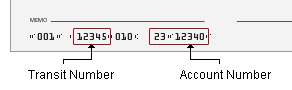

You'll find your transit number at the bottom of your cheque or in online banking.

You'll find your account number at the bottom of your cheque or in online banking.

Contribute to a TFSA that you already hold.

Your existing TFSA account number is the account that holds your TFSA certificates.